Is Y Combinator Worth it by Numbers?

As usual, two times a year for a week the start-up and VC community is burning on the topic of whether the Y Combinator is worth it: VCs are arguing that giving away 7% for around $1.8M post-money valuation is a pure robbery. Maybe it is. Or maybe not, considering the efforts YC invests in the deal flow, selection, and reputation.

Start-ups, on the other side, evaluate whether they should exchange the 7% share wastefully for an over-populated batch where partners hardly have enough time for every single start-up, and hardly have enough expertise in every niche to provide something more than general start-up-building advice. On the other hand, YC doesn’t need to have expertise in every single niche. That’s a start-up’s job to be an expert in its niche. YC’s job is to help with the right alignment to ignite growth and help with the next round of fundraising. YC doesn’t hold a start-up’s hand and doesn’t build a business for it. Anyway, start-ups hope that the demo-day pump will be a good enough compensation for the shares Y Combinator gets. Maybe it will. Or maybe not.

In general, I won’t dive into the biases of either side — each has enough of them. What I’ll try to do is to provide fair comparable numbers for 3 different scenarios and different seed round valuations for each one.

Is it even 7%?

What always surprised me were talks about the 7% Safe. It’s like announcing winners and losers in a race immediately after the start and before anybody even runs half a distance. The thing is 7% Safe is just Step 1 in a priced round when YC’s shares convert — and there are 3 steps.

Any evaluation should be made only after Step 3. In other words, after the Safes conversion in a priced round, mandatory creation or increase of the stock option pool with YC’s share dilution, and after a VC investment into the priced round — again, with YC’s share dilution. Properly speaking, I was pleasantly surprised that Y Combinator agreed for the priced round itself, and the creation or increase of the stock option pool to dilute YC’s ownership.

So, not only is there no reason to discuss the 7% number but the resulting share left of 7% after the dilution in the priced round is different for different valuations and the size of share a new investor gets.

Going further, I’d say that it’s not worth thinking about how big or small a share Y Combinator gets at Step 3 since there is also the mandatory stock option pool and a new VC share. The main number to compare that’s significant for founders is how big a share they are left with after the priced round is done.

Scenarios

Let’s consider 3 different scenarios with Pre-Seed and Seed rounds where Pre-Seed is the initial YC’s investment and Seed is the priced round that triggers Safes conversion:

- Standard Y Combinator’s deal with initial $500K Pre-Seed investment: $125K (7% Safe) + $375K (MFN Safe) that convert into shares at the next priced VC Seed round;

- Scenario without participation in Y Combinator when founders are mature enough and do not even need the Pre-Seed money. They bootstrap and raise Seed round themselves;

- Another scenario without participation in Y Combinator but this time with the requirement of both Pre-Seed and Seed money. I’ll consider a $2.5M post-money start-up valuation for the Pre-Seed round and three sub-scenarios:

3A. $125K Pre-Seed investment;

3B. $250K Pre-Seed investment;

3C. $500K Pre-Seed investment—the same as YC’s one but at a $2.5M post-money valuation.

It should be mentioned that in EVERY scenario there is a step of the stock option pool creation mandatory by any investor. Let’s consider its share to equal 10% of the post-money valuation — usually created right before a VC invests any money: this way a new VC’s share isn’t diluted by the creation of the stock option pool.

Three $10M valuation scenarios

To make comparison easier I modeled cap tables for every scenario the way for similar valuations of a start-up to have similar cumulative investments it receives. This way all we are left with is to compare how big or small the founders’ share is and how its size is compared in different scenarios.

For the sake of simplicity, I didn’t add Y Combinator’s participation right to purchase up to 4% of the new money securities issued in the financing since it might or might not happen, there is no set percentage, and it influences new investor’s share, not the founders’ one.

So, let’s crunch some numbers. Here are 3 mentioned scenarios with a $10M Seed round post-money valuation in each and $1.5M cumulative investments in a start-up in each. (Here is the Excel file)

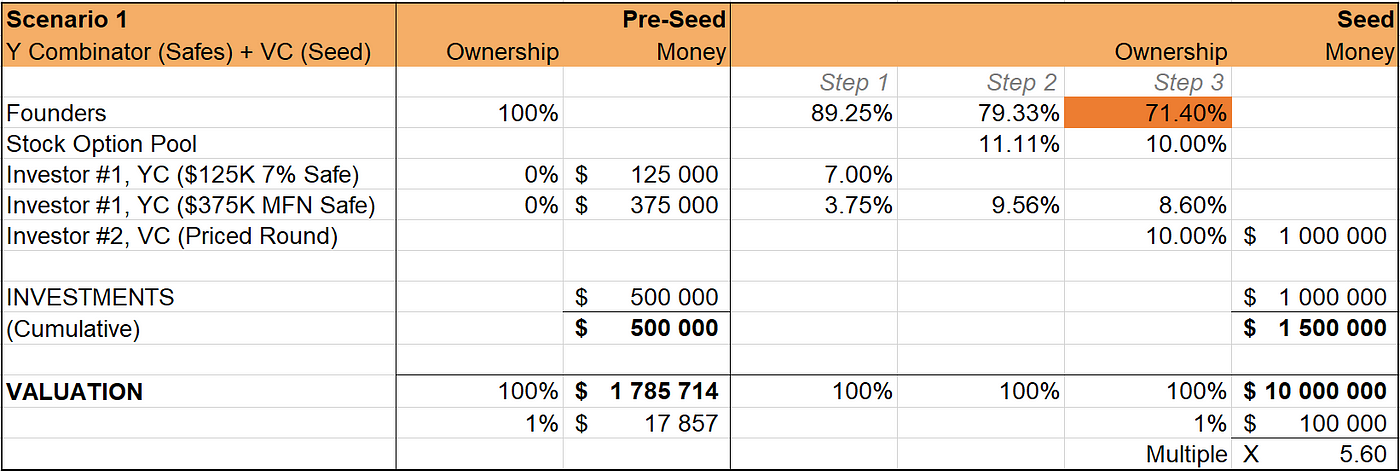

Scenario 1: Participation in Y Combinator’s program ($500K Safes).

Properly speaking, based on the Y Combinator’s deal structure it’s reasonable to consider the first $125K Safe as a 7% Pre-Seed investment and additional $375 MFN Safe as participation in the next Seed round. You just receive $375K in advance but it’s a part of the next Seed round’s structure.

Scenario 2: Founders don’t participate in YC and go straight to the Seed round.

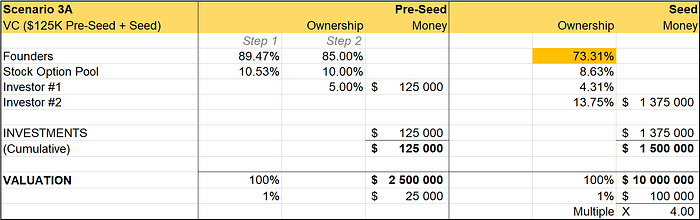

Scenario 3A: Founders raise both Pre-Seed and Seed rounds on their own without participating in YC’s program. The Pre-Seed investment is $125K.

This scenario is very close to Y Combinator’s deal if we consider that YC’s $125K Safe is basically a Pre-Seed round but with ~$1.8M valuation.

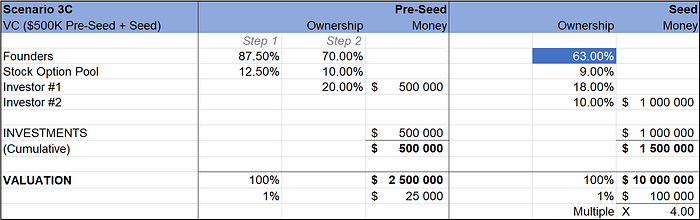

Scenarios 3B and 3C: Founders raise both Pre-Seed and Seed rounds on their own. The Pre-Seed investments are $250K and $500K respectively.

It’s obvious that the most favorable scenario for founders is the one where they don’t raise the Pre-Seed round and go straight to the Seed. They keep 75.0% of the company (Scenario 2). If they raise just $125K in exchange for 5% of the start-up (Scenario 3A), they keep 73.31%. Less favorable but I’d say reasonable is acceptance into Y Combinator when founders are left with 71.4% (Scenario 1). Scenarios where founders first raise Pre-Seed round of $250K (Scenario 3B) with 70.0% left or the same $500K as Y Combinator provides (Scenario 3C) with 63.0% left and then raise Seed at the same $10M are the least favorable.

In general, the smaller the share founders let go in the Pre-Seed round, the better it is. E.g., if start-up gives just 5% in the Pre-Seed, the deal is a little better than with YC’s 7% virtual Pre-Seed: (73.31% vs 71.4%). Though, it’s hard to compare the intangible value Y Combinator provides.

All scenarios, all valuations

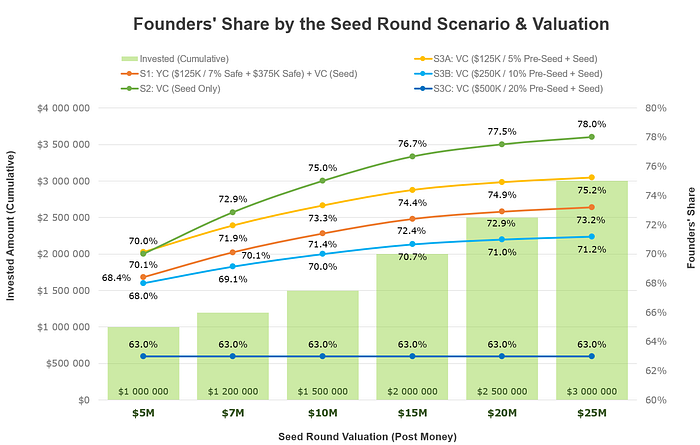

For each scenario I created variants with different post-money valuations of the priced Seed round: $5M, $7M, $10M, $15M, $20M, and $25M — yes, they say that YC start-ups could be valued that high at the demo-day.

Now let’s run the above calculations for every valuation option.

So, is Y Combinator worth it?

Now it’s possible to evaluate what founders are left with for each scenario and each priced round option. If we take the $10M valuation option we’ll see that founders get only 3.6% less ownership in case they participate in the Y Combinator’s program with enormously more chances to be introduced to the top Silicon Valley VCs, leverage their FOMO, and get the deal (Scenario 1: 71.4%) than trying to raise at $10M post-money entirely on their own without having any money invested in the start-up before the Seed round (Scenario 2: 75.0%).

What’s even more interesting is that the situation is much worse in Scenario 3C when founders raise on their own a Pre-Seed round with the same money Y Combinator provides to its participants. It’s a staggering 8.4% less ownership (Scenario 3С: 63.0%) than in the result of the YC’s deal (Scenario 1: 71.4%). So, only Pre-Seed that loses just 5%―less than YC’s 7% — would result in more ownership than Y Combinator’s deal (Scenario 3A: 73.3%).

I’d say there are significantly more chances for a start-up to end up with less ownership than the Y Combinator’s deal in Scenario 1.

I believe there are enough mature smart founders who don’t need Y Combinator. The only question is what valuation of their start-up they could reach on their own without any prior investments or with a Pre-Seed round that takes less than 7% and without the help of Y Combinator’s reputation and community. Could they get to $10M, $15M, or $20M on their own?

If the answer is “yes”, they definitely can make it without Y Combinator.

If the answer is “no”, well, Y Combinator is definitely worth it.

P.S. A caveat about Y Combinator’s Safe instrument

It’s important to stress that the YC’s deal is only good as long as a priced round follows it. Due to its structure, the Safe is very aggressive in anti-dilution protection. It is the post-money Safe. In other words, it offsets to founders any possible dilution by any additional Safes or convertible instruments issued after the Y Combinator’s investment and before a priced round. While follow-on financing should dilute previous financing shares, YC’s Safe converts after all the Safes and convertible instruments that followed it have converted in conjunction with the priced round. So, the follow-on financing dilutes founders only — not Y Combinator — even if YC’s financing happened earlier. If you participate in the Y Combinator’s program, make sure the following financing is a priced round.